As a result of the inferno in Los Angeles County unfold this earlier week, inflicting 10 deaths, 9,000 destroyed buildings and 35,000 scorched acres up to now, consultants moreover feared it is exacerbating a home insurance coverage protection catastrophe gripping California and much of the nation.

AccuWeather estimated Wednesday that full damages will exceed $52 billion, with estimates of insured losses $20 billion. By Friday, AccuWeather elevated virtually tripled its full damage estimate, to quite a lot of $135 billion to $150 billion.

Whereas the fireplace’s unfold was being contained in areas lastly, the Santa Ana winds preserve whipping all through the bone-dry Los Angeles area, whose conventional winter moist season certainly not arrived, transporting embers to ignite neighborhoods and hillsides. The Pacific Palisades, Eaton, Hurst and Sunset fires proceed to burn and are solely minimally contained.

“This is not a typical pink flag alert,” talked about Los Angeles County Fireside Division Chief Anthony C. Marrone at a data conference. “L.A. County and all 29 fire departments in our county mustn’t prepared for any such widespread disaster.”

Neither is the insurance coverage protection enterprise. Suppliers have been already in catastrophe mode over its coping with pure disasters that many think about are the outcomes of native climate change, lots so as they chose to tug once more on offering insurance coverage insurance policies or abandoning at-risk areas altogether. This latest disaster is susceptible to see further requires reform and for model new fashions to help property homeowners get higher their losses over extreme weather-related incidents. The problem of native climate change will undoubtedly be entrance and center in these discussions.

Age of catastrophe

Extreme local weather events and catastrophic losses mustn’t a California-only draw back. Only a few months previously, Hurricane Milton pummeled Florida, inflicting higher than $100 billion in full losses along with an estimated $34 billion in insured losses. Two weeks earlier Hurricane Helene and its floods racked up damages of $59 billion, according to the North Carolina State Funds Office, solely 1 / 4 of which was insured. Insurers have retrenched in all places within the nation, mountaineering premiums or not renewing insurance coverage insurance policies and leaving some states altogether.

The U.S. Senate Banking Committee launched a report ultimate month discovering that the home insurance coverage protection catastrophe has unfold to 17 states, whereas the share of non-renewals rose in 46 states in 2023. House owners in Oklahoma, Iowa, South Dakota, New Mexico, Nebraska and elsewhere have joined these in Florida, Louisiana, California and North Carolina scrambling for insurance coverage protection.

Within the meantime, insured losses because of “U.S. pure catastrophes” hit $109.6 billion in 2022, a few twentyfold enhance from $4.6 billion in 2000, according to the Insurance coverage protection Commerce Institute. Globally, damages from extreme local weather totaled $320 billion in 2024, of which $140 billion have been insured losses, according to Munich Re, numbers that double the frequent annual losses over the past 30 years.

Proper right here’s what’s being tried to unravel the insurance coverage protection debacle in California, and what’s actually helpful:

As of Jan. 1, California carried out new guidelines to attract insurers once more to the state. In its Sustainable Insurance coverage protection Method, California now permits property-casualty insurers to calculate premiums based mostly totally on fashions of future catastrophic risks, not merely historic catastrophic risks, and to incorporate their reinsurance costs into their premium formulation. In alternate for these carrots to the enterprise, California regulators require insurers to increase underwriting in wildfire menace areas in a formulation based mostly totally on a share of their market share inside the state.

Provide: California FAIR Plan Property Insurance coverage protection

The hope is these modifications may help shore up the FAIR Plan, the insurance coverage protection of ultimate resort proper right here that’s funded by private insurers and their shoppers.

Will these modifications work to stabilize the market?

“We have been very supportive of the reforms and suppose they’ll stabilize the market. The necessary factor one is to allow catastrophe fashions to enterprise forward in its place of attempting backward,” talked about Seren Taylor, vice chairman for the Personal Insurance coverage protection Federation of California. Already Allstate Insurance coverage protection launched in December it might resume writing quite a lot of sorts of residence insurance coverage protection insurance coverage insurance policies inside the state.

Nevertheless unbiased consultants and shopper groups have fully completely different opinions.

“Throughout the fast time interval, these regulatory modifications will allow insurers to jot down further insurance coverage insurance policies and incentivize their return to the market,” talked about David Jones, director of the Native climate Menace Initiative on the Center for Laws Energy & the Environment on the School of California Berkeley Laws School and a former California Insurance coverage protection Commissioner.

“Nevertheless in the long term we’re not going to outrun native climate change with insurance coverage protection price will improve,” Jones talked about. “We’re not going to have the power to cost hike our means out of the catastrophe.” He cited the experience of Florida, which allows future catastrophe modeling and reinsurance costs in premium formulation nonetheless which has a excessive insurance coverage protection scarcity and affordability draw back. “Florida has completed the whole thing insurers have requested for in California. However in Florida, nationwide insurers are nonetheless not writing insurance coverage protection,” he talked about, “and prices are 4 events the nationwide frequent.” Florida had the easiest non-renewal cost of any state in 2023.

“I imagine the tragic Southern California fires are one different sad outcomes of our failure to cut back burning of fossil fuels and transition fast adequate to a low carbon monetary system,” he talked about, noting the abnormality of the terribly dry circumstances in what’s Southern California’s moist season.

Mike DeLong, evaluation and advocacy affiliate for the Shopper Federation of America, talked about, “We’re not a fan of Commissioner (Ricardo) Lara’s Sustainable Insurance coverage protection Method. We don’t suppose it’s going to work for patrons; it obtained’t make insurance coverage protection further moderately priced and accessible.” He talked about future catastrophe modeling “usually is an effective issue,” nonetheless fashions need larger data.

What may fit to unravel the problem?

“Most importantly, we’ve got to switch sooner to transition the monetary system away from fossil fuels, which can be a very powerful contributor to greenhouse gases that drive native climate change, which drives extreme local weather disasters” talked about former Commissioner Jones, citing this as essential change needed. These local weather disasters are inflicting deaths, property destruction and supreme insurance coverage protection price hikes and absence.

Secondly, he talked about, property homeowners, communities and governments should actively mitigate menace by hardening properties and thinning forests and landscapes. Thirdly, insurers should reward them for mitigation. In underwriting alternatives, insurers don’t for the time being account for mitigation.

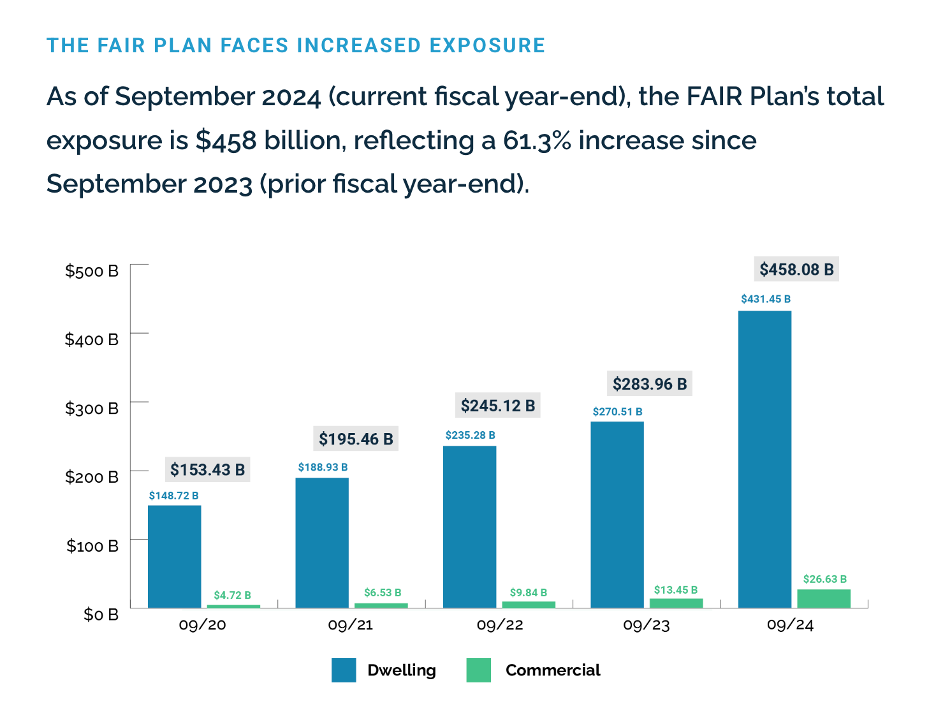

Lastly, California should shore up its FAIR Plan. In accordance with its web page, the FAIR Plan’s full insurance coverage protection publicity rose 61 % in a single 12 months, between September 2023 and September 2024, as further house owners use FAIR for insurance coverage protection. A San Francisco Chronicle analysis found FAIR insures $24 billion in properties inside the zip codes now burning, nonetheless the Plan has solely $385 million in reserves.

Totally different ideas to help treatment the insurance coverage protection catastrophe embody asking insurers to be part of the reply in its place of part of the problem. Most insurers are massive merchants in fossil fuels each by underwriting fossil fuel duties or investing in fossil fuel equities and debt. A study by Ceres, ERM and Persefoni of the belongings of giant U.S. insurers found insurers held $536 billion in fossil fuel belongings in 2019. State Farm Insurance coverage protection held huge stakes in tar sands and coal investments — the two dirtiest and most dangerous of fossil fuels.

State Farm was moreover the first massive residence insurer to stop renewing California insurance coverage insurance policies.

[You’re leading change in an unpredictable environment. Get the strategies you need from the world’s top sustainability leaders at GreenBiz 25, Feb. 10-12, Phoenix.]